CONTENTS: 1 - THE PROPERTY CLOCK’S EXISTENCE, 2 - GROWTH, 3 - YIELD, 4 - PROPERTY PRICES: ACTUAL PRICES, REAL PRICES & BUBBLES, 5 - 12PM TO 3PM (HOTSPOT), 6 - 3PM TO 6PM (COOLING SPOT), 7 - 6PM TO 9PM (COLD SPOT), 8 - 9PM TO 12PM (WARM SPOT), 9 - STRATEGY SUMMARY, 10 - LIFETIME PROPERTY CLOCK, 11 - INTERACTION BETWEEN THE PROPERTY CLOCK AND THE LIFETIME PROPERTY CLOCK

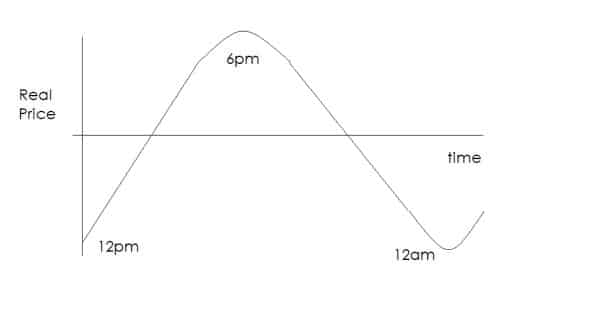

So lets look at the property price curve again:

So at 12pm we can see that the property price is at the lowest point below the real price. Now in order to find out if you have found an area that is in the 12pm to 3pm range you need to compare the real price with the actual price the property can be bought for. So the two key figures in all of this are:

So at 12pm we can see that the property price is at the lowest point below the real price. Now in order to find out if you have found an area that is in the 12pm to 3pm range you need to compare the real price with the actual price the property can be bought for. So the two key figures in all of this are:

- The actual price

- The real price

If the actual price is less than the real price then BINGO!

The actual price

We determine this as being 95% of the advertised price of a property. As an average properties sell at 95% of their asking price. So for example if we see a property advertised for £60,000 then the actual price will be:

£60,000 x 95% = £57,000.

In reality the actual price is the price you can get the property for. It could be 95%, 100% or even 105% of the asking price dependent on how competitive the market is. However, under normal conditions 95% is about average.

The real price

The real price of a property is based on fundamental principles. The fundamental principles that apply to the property price are:

The greater of:

- The price willing to be paid by an investor

- The price willing to be paid by a first time buyer

So whichever is greater out of these two figures will be the real price of the property. So we need to calculate both of these prices.

The price willing to be paid by a professional investor

The price willing to be paid by an investor will be function of what he could get elsewhere in the market. If an investor wished to take no risk then he could stick the money in the bank and earn interest. If he were to invest in property he would look for a premium as he was taking on risk. As property is a long term investment he would look for a comparison of the same timescale that is risk free. The best rates you would get would be from a:

20 year fixed interest government gilt

A government gilt is a loan to the government. As it is assumed that the government will not go bankrupt we can assume that it is risk free. Property is considered to be the next lowest risk investment out there. As an average property investors require a minimum of 2% loading on a 20 year fixed government gilt for them to invest. This will determine the yield required and hence set the real value of the property. Lets look at an example:

Variables:

20 Year Fixed Interest Government Gilt 5.62%

Property Investor Loading 2.00%

Annual Rental Value of Property £5,000

The real value would be:

£5,000 x 1/(5.62%+2.00%) = £65,616

This will be the maximum value an investor would be willing to pay for a property with a rental value of £5000. If the property price was higher then the investor will place it in a risk free investment like a government gilt. The property price could be higher due to a first time buyer being able to afford the property.

The price willing to be paid by a first time buyer

The price willing to be paid by a first time buyer will be:

His salary x 4

(0.95)

This assumes that lenders will lend 4 times his salary if he puts down a 5% deposit on the property. So, in the same example above, if a first time buyer wants the same property and his salary is £21,000 then he could afford a purchase price of:

(£21,000 x 4)/(0.95) = £88,421

So in this example the first time buyer ‘wins’ and thus the real value of the property is £88,421.

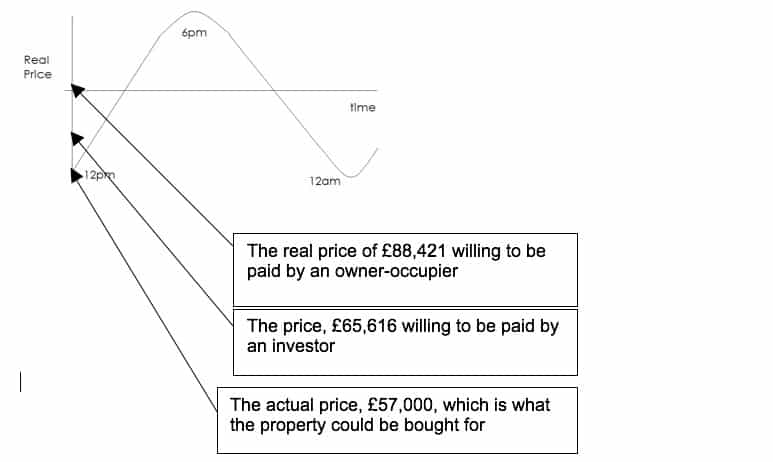

So looking at the actual price compared to the real price we have:

Actual price £57,000

Real price £88,421

Under-valuation £31,421

Looking at it split between the investor and the owner-occupier:

| Owner-occupier | Professional Investor | |

| Actual price | £57,000 | £57,000 |

| Real price | £88,421 | £65,616 |

| Under-valuation | £31,421 | £8,616 |

So we can see clearly that we are within the 12pm to 3pm quarter. This is because both the investor is interested as well as the owner occupier due to the prices willing to be paid by each are above the actual price. We can see that the owner occupier has more to gain in buying than the investor so aggressive bidding will occur thus pushing the price up quickly and dramatically. Looking at it in relation to the property price graph:

So we can see who drive property prices – We all do! Its our attitude that drives a property price NOT interest rates – even though all the city analysts believe that it does so. Interest rates do play a part but its our propensity to borrow, the availability of borrowing, the willingness of lenders to lend and our fear of missing the boat that causes prices to rise.

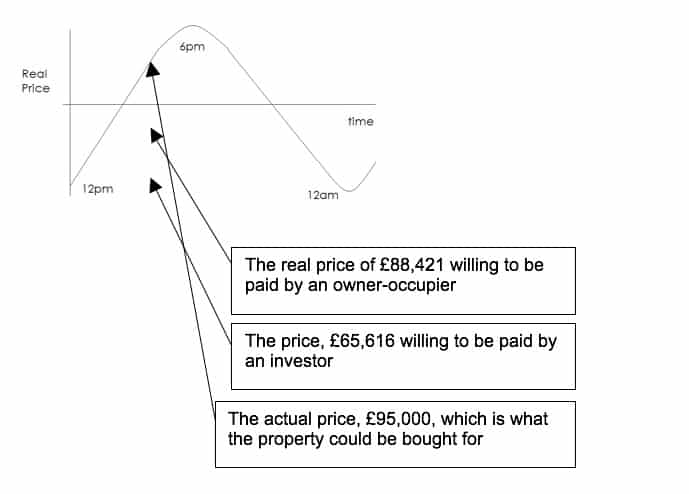

So what is happening between 3pm and 6pm. Well effectively properties are being sold above the asking price. Using the same example above lets say asking prices have rocketed to £100,000. Then we would have the actual price as:

95% x £100,000 = £95,000

Both the professional investor and owner occupier prices will remain the same as nothing would have changed. That is to say over the period of rocketing property prices the following would have remained stable:

- Gilt Rates

- Salaries

- Rental Value of the property

- Lending criteria by the banks

So we would have the following table:

| Owner-occupier | Professional Investor | |

| Actual price | £95,000 | £95,000 |

| Real price | £88,421 | £65,616 |

| Over-valuation | £6,579 | £29,384 |

This over-valuation is what I call the bubble element to the actual property price. Specifically the bubble element is £6,579 as it will be the lower of the two over-valuations. So in this case it is the owner occupier because an owner occupier has a higher valid bid price than the investor.

Looking at the graph again:

So who are buying at £95,000? Well it certainly ISN’T the:

- Professional Investor or

- Standard Owner Occupier

The people that are buying at inflated prices are:

- The speculative investor – This investor is banking on prices rising at the same rate as in the past. Also if the stock market is under-performing then the attraction of the property market is heightened. He can buy and sell within a number of months or years and make a tidy profit. This type of investor can make money if he knows when to sell but he will only be selling to another speculative investor or ……….

- The scared owner occupier – This type of owner occupier is scared of prices rising beyond affordability so he buys a property for more than what its worth. i.e. a professional working couple buying an unsuitable property to live in like a studio flat or an ex-local authority 1 bed flat. They should wait for prices to fall so they can get a 2 bed flat but their fear makes them buy a smaller property for an inflated price.

- The over borrower – This type of buyer will buy by using a deposit that has been raised by borrowing from a bank, credit card or loan company or get a self-certified mortgage where they lie about their income. Either one of these strategies results in over-borrowing.They also think, like the scared owner-occupier and speculative investor, if they do not buy now they will miss out.

The best way to spot a bubble element is to calculate it. The equation holds:

Pactual = Preal + Pbubble

Pactual - The actual price of the property defined above

Preal - The real price of the property defined above

Pbubble – The difference between the actual price and the real price

So the bubble element exists when the actual price is greater than the real price. To spot bubble elements look at:

| What to look for | Why |

| Type of property | If you’re buying a studio flat for the price equivalent to 5 times the salary of the typical purchaser then a bubble element may exist as the property you are buying is unaffordable to the typical purchaser. It may not have a bubble element if the rental value stacks up – see below. |

| Type of purchaser | If you are considering to buy a small 1 bed flat that’s in a city centre then consider what the average salary is for a worker in that city centre. Calculate what the average city worker could afford as they will be your main buyer as they invariably pay more than an investor. Can the city worker afford what you are paying? If they can’t then you may be buying at an artificially high price unless it has a decent rental value – see below. |

| Rental Value | What does the property yield at? If the property yields greater than a 2% loading on the 20 year gilt rate then its priced correctly. If it yields below then there may be a bubble element to the price. |

| 2nd & 3rd time buyers | Bear in mind that people move up the property ladder and so there is a gain from the sale of their original property which contributes to the overall purchase price. If you are buying a 2 bed home then it may be a second-time buyer that is the typical purchaser of this property. The real value will be 4 times their salary PLUS the estimated gain on their previous property. If you are paying more than what they can afford then a bubble element may exist. |

| AWARENESS TABLE FOR CHAPTER 4 | |

| 20 year government gilt figure

| Being aware of this will make you able to calculate the real value of the property as the real value is a function of a 2% loading of this rate. |

| Differential between long term rate and current rate | If there is a significant difference between the long term rate and the current rate then the property prices can abnormally rise or fall from their real property value. At the minute there is nothing to worry about and the differential is reducing. However close inspection of the differential will keep you ahead of the pack as you will see how the lenders react and how property prices change. Also be aware of heavily discounted mortgage products coming to the market. They can distort prices if these deals become popular forcing other lenders to reduce their rates and making the whole mortgage market even more competitive than it already is! |

| Rental Value of Property | For you to really exploit all the possible opportunities then you need to be aware of the rental values of property. Based on this you can calculate the real value of a property in conjunction with your required return which you can then compare to the actual asking price. If the real value is in excess of the asking price then take a look at the property! |

| Current Market Value of Property | For you to really exploit all the possible opportunities then you need to be aware of the current market values of property. This involves searching on the net, looking in local papers and talking to estate agents. Based on your real value of property calculations you can see if the current market values look attractive. |

So in the last 4 chapters we have set out the basis for the property clock. Now lets get in to the detail of each quarter.